For over 20 years, Knight Frank has partnered with CACI to achieve a long-term vision of becoming the world’s leading independent property advisor. Knight Frank works with various industries and businesses on their property and location planning strategies. Accessibility to reliable and accurate information to successfully serve clients and the ability to build authority as a market leading commercial agent have remained at the business’ core throughout.

Despite Knight Frank’s wider recognition for its work within residential property, the business is evenly split between residential and commercial real estate. In recent years, the general climate surrounding realty has become increasingly challenging, with macroeconomic conditions weighing heavily on this industry globally, particularly in terms of capital market investments. To manoeuvre these challenges, Knight Frank has been using CACI’s GIS software, InSite, along with various CACI datasets such as Acorn, the UK’s leading geodemographic segmentation tool.

The Challenge

Knight Frank’s primary challenges have been twofold:

• Determine how to navigate ongoing global uncertainty in the real estate industry.

• Handle volatility in capital investment markets.

Stephen Springham, Head of Retail Research at Knight Frank, elaborated on the impact that these challenges have had on the business.

Stephen explained:

Capital market investment is key to real estate markets and obviously that is probably at the sharpest end of economic sentiment. Investor sentiment isn’t sky high at the moment, so that is probably the biggest barrier we have to overcome, although we’re probably not radically different from most global companies in that regard.

The Solution

CACI’s InSite software has significantly supported Knight Frank’s business endeavours through both the nationwide insight from Acorn, as well as the shopper understanding from the machine-learning

catchment model, Retail Footprint. “It’s a window to the world of data. A lot of those datasets are bespoke and unique to CACI,” Stephen explained.

Additionally, CACI’s business consultancy solutions and thought leadership have been supporting Knight Frank in improving their overall business functions by supplying the business with the necessary tools to effectively advise retailers and support due diligence regarding buying and selling within the capital market.

The Results

According to Stephen, there has been a noticeable uptake across the business in data usage, with several transactions on shopping centres Knight Frank completed over the course of last year that were achieved

thanks to the support of CACI’s data and InSite tool.

One of the business’ recent and most notable acquisitions came in 2021, with Knight Frank acting for Redical in the purchase of the Victoria Gate/Victoria Quarter Shopping Centre in Leeds. This £120-million deal was executed in part through a deep dive of data provided by CACI’s InSite tool.

The Future

While Knight Frank continues to have an open dialogue with CACI on any new developments or datasets that could continue to support the business’ initiatives, CACI’s InSite and data have created a notable foundation.

How does a challenging economy affect consumer choices and priorities that shape the UK market for elderly care?

It’s no surprise that the cost of living squeeze is having an impact on elderly care operators. Private residential and domestic care cost money: consumers are looking for ways to economise. Older people want and need comfort and care as much as ever, but they and their families are tightening their belts. Inevitably, they’re considering the cost of different care settings and options.

What does this mean for residential and domiciliary care providers? It’s early days, but as for every other consumer sector, you need to be prepared for the market to change. A proactive approach to understanding current and future customers and modelling potential demand in your locations can uncover opportunities to maintain occupancy and optimise your services to match evolving priorities and needs.

If you don’t have a crystal ball to hand, that may sound like a tall order. But knowing and anticipating market demand in your locations doesn’t depend on magic or guesswork. Consumer and location data together provide reliable evidence that can help you identify ways to stay relevant, accessible and financially stable.

Not all groups are impacted to the same extent by the rising costs of living. The majority of Acorn Groups still have a sizeable disposable income despite the recent 5% average fall. Source: CACI Paycheck Disposable Income 2022 v2

Despite the bleak headlines, the economic impact varies considerably for different household types and in different areas. Many older consumers still have savings, disposable income or assets that allow them to choose the care they want. If you can understand the profile of your current and future customers in detail, it’s easier to identify and reach out to local prospects.

Location intelligence data is a well-established source of insight for care home operators and domestic care providers that are considering expansion or new sites. Mapping the age and affluence of the local population in a potential catchment helps to indicate where there’s likely demand for elderly care services.

But alongside age and income, there’s a lot of more subtle data that can help you market your existing services, confirm or reshape your propositions, benchmark your pricing and adjust the range and type of services you offer. This type of insight is extremely useful in a fast-changing market.

CACI data insight can answer crucial questions about your customers and market:

• What are the characteristics of your local and target customers?

Acorn profiling groups UK consumers by affluence, life stage and priorities

• What are your current and potential customers thinking, feeling and intending to do differently? Quarterly Consumer insight surveys of the UK population • How has customer spending on different outgoings changed?

Transactional spending data shows the split of spend with different brands and operators • Whose disposable income is affected?

Postcode model of income in different locations, showing how it’s being spent. • What’s around the corner?

Dynamic modelling forecasts what could happen to consumer spending if inflation, fuel and other costs rise in a range of different ways

CACI’s current disposable income model reflects the changes we’ve observed in the last few months. Although all households are affected by rising costs, the majority of our Acorn consumer profile groups still have a significant disposable income. It’s groups like Student Life and City Sophisticates that have seen the largest decline, driven by property costs.

There has been major growth in spend on private healthcare, with a wide range of demographics prioritising health over other non-essential spending. Source: CACI Transactional Spend, June 2022

For elderly care operators, it’s encouraging to note that Comfortable Seniors, Countryside Communities and Successful Suburbs, who are likely to form far more of the target market, have some of the highest levels of disposable income, reflecting smaller or non-existent mortgages, good pensions and comfortable savings accrued over previous years.

Spending on private healthcare has increased in the past year. The Covid-19 pandemic and concerns about NHS waiting lists are driving this change in priorities for households across most Acorn groups. Despite rising essential costs, many consumers now regard healthcare expenditure as a necessity, not a luxury. This could have a positive impact on perceptions of value in elderly care.

These are just the headlines from our latest national data. Every elderly care provider has a different operating model and works in unique locations. CACI’s health and social care team can select data and build customised reports that directly reflect the opportunities and changes happening in your catchment areas today and tomorrow. For mid-sized operators, it’s vital decision-making information to inform strategy and tactical decisions that will help your business compete and thrive in a challenging economy.

We can help you:

• Continuously analyse, monitor and adapt – stay ahead of policy and new competitors when finding new customers and recruits

• Tailor marketing engagement and recruitment key messages to reflect the requirements of local potential pools of customers and staff

• Understand your staff and customer base and how its segments are impacted by different cost of living challenges, to identify risk and opportunity

• Tailor your offer to changing consumer and staff requirements

CACI’s specialist elderly care and senior living team work with clients in the UK and internationally to help them improve operational and financial performance with access to vital insights into their customers, employees and locations.

Over the last three years, we have seen a more significant shift in consumer habits than we could have imagined. Currently challenged by the rising cost of living and an economy in recession, the post-pandemic spending bubble was cut much shorter than initially anticipated by economists.

Like everyone in January, CACI reflected on the last few years, and as part of this, we revisited predictions that we made during the height of the Covid-19 pandemic. Consumer behaviour changed significantly in the space of several days, triggered by widespread temporary store closures during the lockdowns. Some stores were never able to reopen; whilst online platforms boomed, in light of these significant behavioural shifts, CACI rebuilt predictions to reflect this new normal.

How close were CACI’s consumer online spending predictions to actual results?

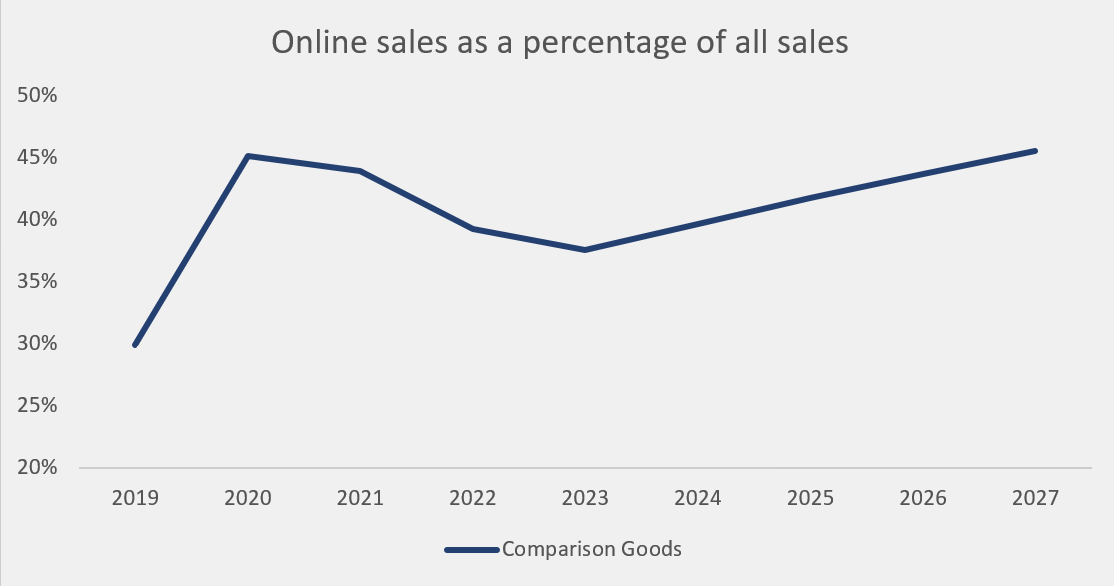

Mirroring our spend predictions, a phrase we maintained at CACI at the time was that “online spend jumped forwards five years in one month”. What we have come to realise was that three years on, these spend predictions, shown in the below chart, highlighting a return to in-store, were very close to the true picture.

How can CACI track consumer online spend behaviour?

CACI can unpick these new trends in spend behaviour using our new and exciting tool kit of Spend Dimensions and Brand Dimensions, which tracks over 200 shopping centres and 300 brands across the UK.

What we can see demonstrated in the above chart is a post-pandemic slump in online spend as a proportion of total spend. In 2023, online spend falls to 38%, before gradually rising again in the preceding years.

Whilst the current split in online and offline engagement provides us with an overall national average, it is important not to expect all shoppers to follow suit. We have seen asset type, product category, brand, region and demographics all play a big part in the extent to which a shopper might engage online.

Who is most likely to shop online?

Demographically, the split between those engaging in-store and online has become less distinct, highlighting the closing of the digital gap between young and old, with the difference between online market share across all groups dropping from 10% to 5% over the last year.

However, the big picture doesn’t change. Key online shoppers continue to be younger shoppers across the affluence spectrum as well as more affluent shoppers, likely driven by greater access to e-commerce platforms and the ability to afford delivery costs.

How does this vary by product category?

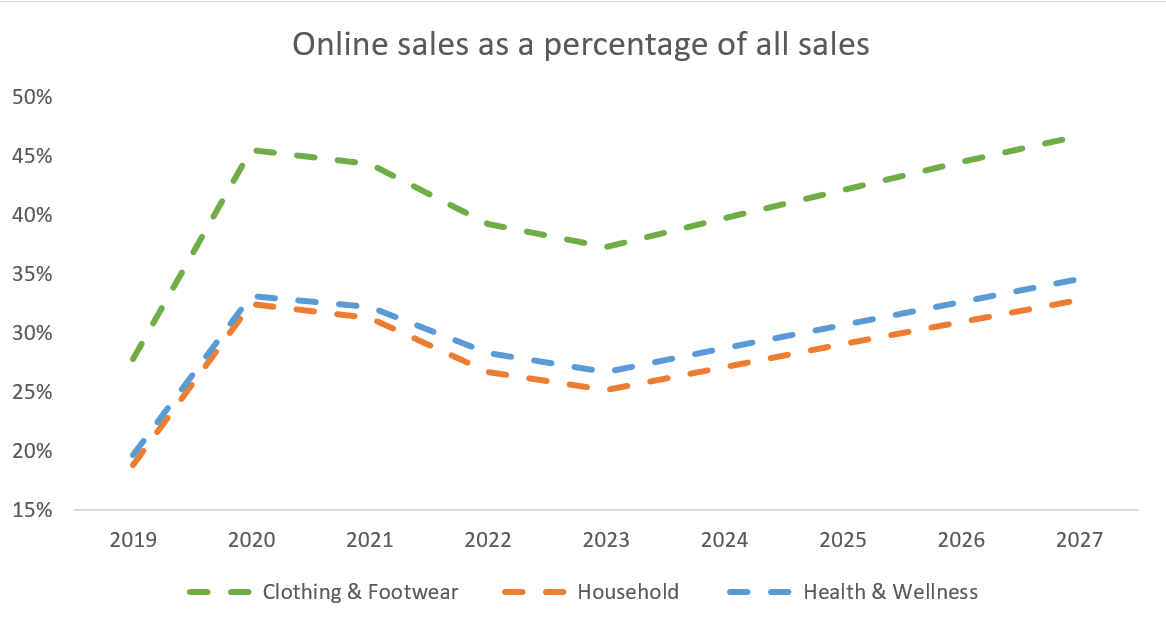

The recent shift back towards in-store engagement isn’t clear-cut and does vary by product category. CACI expectations were that the drivers of the overall return to the store would be clothing and footwear, household and health & wellness brands. This has been the general spend trend that we’ve been seeing across the UK since 2020.

The variation by category gets further exacerbated by the time of year. For example, comparing the months of October to December 2021 and 2022 in the chart below, there was a clear shift for household and kids’ goods spend to in-store, likely driven by the desire to experience before purchasing. Whereas, General Retail painted an interesting picture within the final quarter of 2022. Both in 2020 and 2021, with Black Friday and Cyber Monday taking place in November, Christmas hit online earlier than in-store, boosting online’s share of the market temporarily. In December, our Christmas survey reiterated this sentiment, with over half of those shopping online citing a main drive of this being concern with the rising cost of living and saving money, whereas over half of those shopping in-store did so for the experience. The experience-focused, in-store shoppers drove the resurgence year-on-year of in-store spend in December.

What does the return to in-store mean for retailers?

Across the 300 brands we tracked, many pure online brands are experiencing a decline in market share, in-store brands have typically performed well, and those blended brands have seen a shift towards a greater in-store market share. The power of the store can be seen through brands such as Decathlon, Nespresso, Build-A-Bear and Denby, who have all shifted to greater reliance on the store over the last quarter. In comparison, online disrupter brands such as Vinted and Shein which thrived through the year began to see a drop off.

What does the future of consumer online spending behaviours look like?

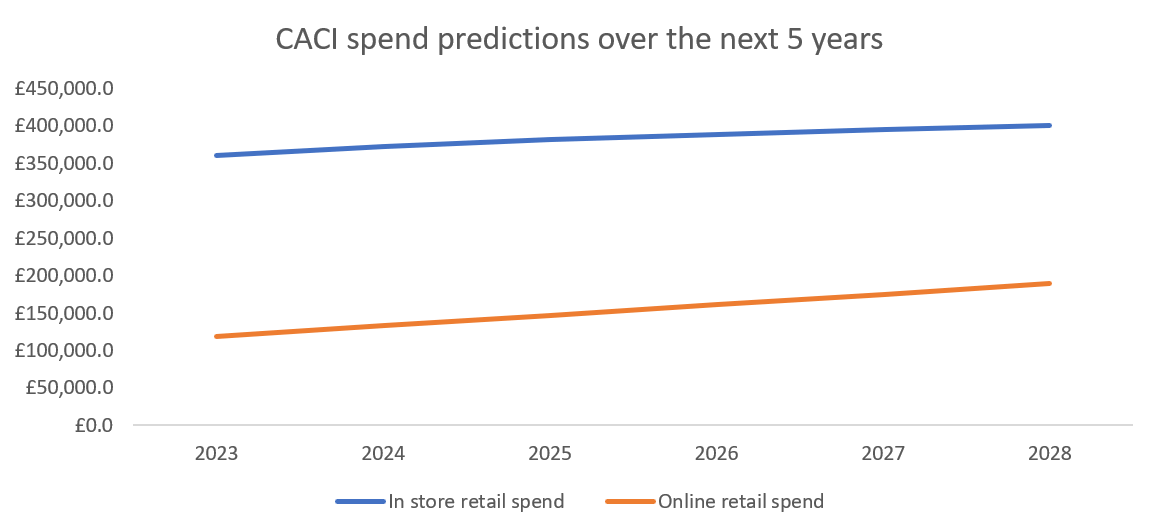

Whilst 2022 did represent a return to bricks and mortar, we are still at least a year ahead of where we would have been if the pandemic hadn’t happened. We expect to see continued growth in both on and offline retail spend, although proportionally online spend will increase.

However, it is undoubtedly true that we are currently, and will continue to, experience unexpected macroeconomic challenges which will impact different brands and destinations in different ways. Brands can no longer rely on their name as we have seen with the casualties of too many well-known landlords and retailers. Therefore, making informed decisions through the use of CACI data will help retain a competitive advantage and stand out from the market.

To learn more about how CACI can help your brand navigate changing consumer spending habits, get in touch with us here.

As the country learns to live with Covid, CACI’s data and consumer research is revealing what the new normal looks like for the nursery market.

Customer Movement is on the Rise

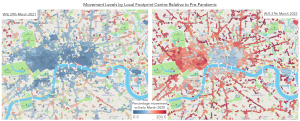

Let’s start with the positives. Remember just how much more freedom we have than we did this time last year. The contrast between the two maps based on anonymised Mobile App data are stark. The map on the left shows movement activity levels in the last week of March 2021 relative to pre-Covid (Early March 2020) for Central London.

Source: CACI / Digital Envoy

Dark blue shading shows areas that movement levels were way down on pre-pandemic across much of London – not surprising given that restrictions were really only lifted in early April 2021 for all but essential activities (albeit including trips to nurseries). The map on the right is the same week this year, and shows swathes of red across much of London, highlighting that activity and visits to many of these areas has returned to almost pre-Covid levels as we learn to live with life after Covid.

Despite the fact that we are seeing record numbers testing positive for the new variant there is no doubt that many are back out and getting on with their lives after a painful couple of years.

New Behaviours and Attitudes

But we have emerged into a different world. The right-hand map shows that the recovery in movement is not universal. There are still clear areas of blue and lighter red in office dominated parts of the city, and around the major stations of London. The same pattern is seen in cities across our county.

Analysis of the data reveals that our city centres are only now returning to something close to what we would have called normal before the pandemic, and transport hubs are seeing visits about 25% down. But regional towns have grown in popularity, with visits up by about 40%. So, clearly we have changed our activities, and it looks like many of these behaviours are set to remain.

Our towns and cities are changing, and we can see it happening around us. But it’s a complex picture. Whilst some have speculated that we are going to witness a long-term boom in the suburbs as everyone moves out of our towns and cities – this is not the case. Despite the jolt that Covid brought there are too many interactions at play for all the old links to be broken.

CACI’s research, carried out as restrictions were eased, revealed that many 18 to 34 year olds, many in the target age groups for nurseries, were keen to return to our towns and cities. These included people from across the demographic spectrum with groups with very different lifestyles – from ‘City Sophisticates’ to ‘Struggling Estates’ in CACI’s Acorn classification amongst those most keen to return to urban living.

Consumers are listing eating out, entertainment and leisure activities as the top reasons for wanting to return.

In short, for many our towns and cities remain places of fun, choice and opportunity – and this hasn’t changed with the pandemic. What we are seeing is that towns and cities are responding to this need. At CACI we have never been so busy in supporting our leisure clients who are busy trying to extend their portfolios, filling the units vacated by retailers hit by the step change in online shopping triggered by the pandemic. And other urban offices and former retail units are being repurposed as urban living – a clear sign that everyone is not heading for the countryside and suburbs.

For many, working patterns look like they have changed for the long-term. Evidenced in the conversion of office space to other purposes and in the areas of blue on the map of central London in worker dominated areas. Our research revealed that workers claim that 2 to 3 days is the optimum number of days they would like to spend in the office, and this seems to be becoming the norm for many. But, it is important to remember that not everyone has this option, including most workers in the nursery sector. It is very easy to think everyone can work from home easily, but affluence, age, location and job role all clearly play a part.

Source: CACI / Digital Envoy

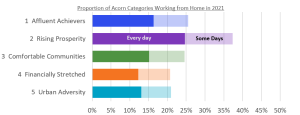

Analysing Kantar’s TGI survey data from 2021 shows that, even in a year scattered with various work from home advice, only 25% of those surveyed said that they worked from home every day, or some days, as their ‘normal’ behaviour.

The chart, using CACI’s broad Acorn Categories to dissect responses, clearly illustrates that it is the ‘Rising Prosperity’ that are most likely to be working from home. These are younger, well educated professionals moving up the career ladder and living in our major towns and cities. 38% of this segment claim to work from home at least some days, and 25% of this is made up of those working from home every day. In contrast only 20 or 21% of lower paid, lower qualified segments ‘Financially Stretched’ and ‘Urban Adversity’ have the luxury of even working from home some days.

Source: CACI / Kantar

As a result of this shift workplace nurseries will no doubt continue to suffer, as many will prefer the flexibility of nurseries closer to home, in line with the shift to ‘hybrid’ working, with many neighbourhood nurseries benefiting from this change. The number of parents requiring nursery spaces is unlikely to be impacted by the rise in home working, as many learnt during the Covid lockdowns that working from home and providing childcare don’t mix. However, many nurseries are likely to see increasing staffing and pricing complexity with parents expecting a level of flexibility that reflects the new-found flexibility in their working hours and location.

So, despite big changes there is no evidence to suggest a need for wholesale changes in where acquisitive nursery groups should be focussing their attention. The big urban to rural shift is not happening and indeed CACI’s research shows that even at the peak of the pandemic 10% of house moves were from villages to towns and cities. Tracking planning applications reveals huge amounts of new dwellings under construction or being proposed in our urban areas and, whilst much of this will have been planned before the pandemic, it’s not that easy to turn a tanker. It is simply not possible for such a shift to happen without fundamental changes in planning policy and housing stock.

So, in summary whilst the change in residential patterns are moderate it is the behaviours of those residents that have changed, and the following are just a few more key behaviour changes that CACI expect to remain:

Communities are eager to stay local

This is good news for nurseries operating well-run community nurseries. But it is increasingly important for nurseries to engage with their wider communities and larger groups need to take care not to look like corporate outsiders

Social governance is increasingly in the spotlight

With consumers expecting their suppliers to behave ethically and transparently

Minimising waste and environmental impact is mainstream

All nurseries now need to ensure that they are meeting parents’ expectations here and that they are living out the values of care for the environment that the children will inherit

Digital is critical to recruitment and engagement

There is no doubt that digital is here to stay – so if you are not happy with your website you can be sure that it is putting off potential customers and if you are not sharing key messages with your parents via emails and portals then you may get left behind

New Challenges and Opportunities

Unfortunately, with inflation and rising rocketing fuel prices, there is no doubt that many families are going to be facing increasingly tough decisions about where to prioritise their spending in the year ahead. This could impact customers’ ability to afford childcare, especially if their salaries rise above the eligibility threshold for free places, but their true disposable incomes fall.

Rising fuel costs for nurseries will compound the challenges of rising wages already driven by the shortfall in staffing that so many in the sector are facing and these need to be factored into nurseries strategic plans.

Successful nurseries should take note of these consumer and market changes, play to their strengths in these areas and they will thrive. But ignore them at their peril as the sector faces the two emerging, and partly inter-related challenges of staffing and the cost-of-living crisis.

We are more aware of our environment than ever before due to an increase in greenhouse gases, holes in the ozone layer, environmentalists protesting on our roads and pollution in our cities. Despite being the 15th best country for air quality and the 6th most environmentally friendly country, our government is under pressure to show that they are trying to improve and meet the ever-stringent environmental targets they are faced with. We all know that it’s the right thing to do, but it comes at a cost to individuals and businesses as we adjust to a new way of life. However, there are ways that we can minimise that cost by being more efficient and planning ahead.

Anyone who has lived in an inner-city area will be aware of the high levels of pollution from vehicles, contributing to lower air quality, especially along busy roads. This increases people’s risk of heart and lung disease and asthma. To help reduce this, local governments are starting to introduce clean air zones where certain vehicles are either not allowed to enter or will be charged a fee for doing so. The aim of this is to encourage drivers to use newer vehicles which meet the Euro VI emissions standard, to purchase ‘zero emission’ vehicles such as those powered by electricity or hydrogen, or to use public transport.

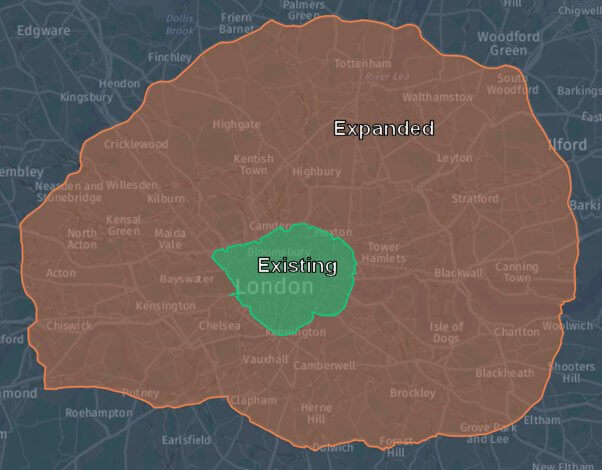

London introduced its first low emission zone in 2008 for large commercially operated diesel vehicles and expanded this in 2012 to cover vans, minibuses, utility vehicles and more. In April 2019 an Ultra-Low Emission Zone (ULEZ) was created, covering the same area as the congestion charge zone in inner London, but applying to a wider range of vehicles including cars and motorcycles.

Vehicles entering these zones have their number plates read by a network of cameras and must either meet the newer emissions standard or the drivers will be charged a daily fee of between £12.50 and £100, depending on the vehicle type.

Since the ULEZ has been launched the London Assembly claims that it has reduced the number of polluting cars driving in the zone each day by 44,000 and that toxic NO2 concentrations have been reduced by 44%.

From 25 October 2021, the ULEZ in London will be significantly expanded from central London to create a single, larger zone up to the North and South circular roads. This is an increase in area of 1,809% (21-380km2) and covers 3.8 million people, compared to the existing ULEZ zone is which covers 203 thousand people.

For drivers of diesel cars older than September 2015 and some pre-2005 petrol who want to enter this zone at any time of day, this means that they will have to pay a daily charge or have to spend thousands upgrading to a newer car. The average price to buy an electric car is around £44,000 – almost 1.5 times the average salary in the UK so this option isn’t feasible for everyone. From a personal point of view, I own a perfectly good 2011 VW Golf diesel, but as the CACI offices in West Kensington are now within the ULEZ zone, this means I’ll have to pay the charge or buy a new car if I want to come into the office.

Car drivers are not the only ones who will be impacted by the expanded ULEZ zone. Delivery drivers, logistics companies and people living in the zones will also be negatively impacted by the changes. Specifically, anyone delivering goods inside London will need to ensure that they are driving a newer vehicle which meets the emissions standards, or they will need to pay the charge. This inevitably will be passed on to customers who will be paying for living in an area with lower pollution.

London is not the only city that is affected by low emission zones. CACI have recently undertaken a study into low emission zones and have discovered that in addition to London there are five other UK cities with low emission or clean air zones currently in place, including Bath, Birmingham, Brighton, Oxford, and York. In addition, a further ten cities are proposing to launch low emission zones in the next couple of years. Some of these low emission zones in these cities only currently apply to buses, taxis, or HGVs, but it is likely that they will be extended to include all vehicles in due course, as has been seen in London.

Comparing the existing and expanded ULEZ zones in London

So, if you’re responsible for a fleet of commercial vehicles, keeping the costs down and also meeting customer expectations – what do you do about it?

Based on the research into low emission zones, CACI have created a dataset of both the current and proposed low emission zones across the country. Knowing the location and extent of these zones is useful in understanding the demographic profile of people living within the areas for marketing and planning, especially as there is likely to be a greater demand for electric vehicles, cycle lanes and environmentally friendly transport solutions in these areas. CACI’s behavioural demographic solutions Acorn and Ocean can help identify households that are likely to be concerned about their environment and those who might be most affected by changes to transport infrastructure.

For logistics companies scheduling deliveries, knowing whether an address falls inside a low emission zone will help calculate any additional delivery charges that need to be applied or determine if that delivery should be served by a more modern, lesser polluting vehicle. If you need to plan for vehicles entering these zones on a daily basis but need to minimise your costs, whilst achieving your carbon efficiency targets, the dataset can be used in conjunction with your route planning software (such as CACI’s Pin Routes), so that the application can identify the roads and customer addresses that fall within the zones, and can plan the routes to minimise the cost whilst still meeting customer requirements.

As the number of low emission zones increases and we are forced to change the way that we travel, we can look forward to a further reduction in air pollution in our cities. However, the significant cost to both individuals and businesses as we change the way that we go about our daily lives is something that cannot be ignored. These environmental challenges are not going away, legislation and environmental targets are likely to become more and more stringent, meaning that we need to put in a solution now.

Monkey Puzzle is the UK’s largest day nursery franchise network, with over 60 nurseries nationwide. For over thirty years, the Monkey Puzzle team has worked closely with parents, staff and Ofsted to deliver childcare of the highest quality, providing children aged three months to five years with unlimited opportunities to learn, develop and grow within a safe, secure and caring environment.

An award-winner in the 2020 Day Nurseries Top 20, Monkey Puzzle is growing strongly. It is always looking for new franchise sites and opportunities, led by a dedicated head office team. Monkey Puzzle also operates a handful of day nurseries directly, providing a benchmark of best practice for franchisees.

The Challenge

Understand the opportunities in franchise locations with enriched local customer insight.

Sophie Hailey is Monkey Puzzle’s Franchising and Property Acquisitions Associate, explains:

Before we engaged with CACI, when we were looking at a new site, the only demographic research we would do was competitor analysis. We would type the site postcode into the OFSTED website and look at comparable sites in a five mile radius. We would mystery shop them to find out about what they offered, the fees and waiting lists, to help us establish a suitable proposition and pricing for our potential new nursery.

When you visit a site, you can get a good feel for a location. This is really important, as is the competitor research, but we needed more information and evidence to back up our decisions, as our network expands. We wanted to give our franchisees confidence as well as committing to the right sites for our model. The more relevant insight we have, the better our decisions can be.

The Approach

Sophie Hailey, Monkey Puzzle’s Franchising and Property Acquisitions Associate talked to CACI about Monkey Puzzle’s franchising and the kind of information that was important in her decision-making process. Acorn and InSite reporting would give Sophie and the team access to valuable customer demographic and local market information to enrich their understanding of new and existing sites and opportunities in the local area. Sophie explains:

The site reports we generate help us to narrow down potential sites quickly – we look at a number of factors about the catchment that tell us whether it’s worth investigating a proposed site further. We can see how close it is to existing sites, so we can avoid cannibalisation, as well as how strong the customer demand might be in the local community and workforce.

The Results

With InSite reporting and Acorn data, Sophie and her colleagues have a clear, shared knowledge base that informs the franchise development process with consistent and up-to-date customer and location information.

Our nurseries are currently gathering postcode information from existing customers, so we can map exactly where they come from in each catchment. This will help us understand our existing customer base better and recommend how to customise the proposition and marketing for different types of location.

Sophie Hailey, Monkey Puzzle’s Franchising and Property Acquisitions Associate