It is now crucial for wealth managers and financial service firms to better their consumer understanding. They can do so by ensuring they are well-versed in the entire consumer lifecycle and journey, understand optimal communication techniques required for effective customer marketing, collect enriching customer-centric data to tailor marketing and distribution effectively, and establish innovative ways of measuring these areas to remain compliant.

Access to insightful demographics on the lifestyles, attitudes and behaviours of investors within the market can help drive improved distribution performance, revenue growth and increased client engagement. This crucial investment market knowledge can be provided by CACI.

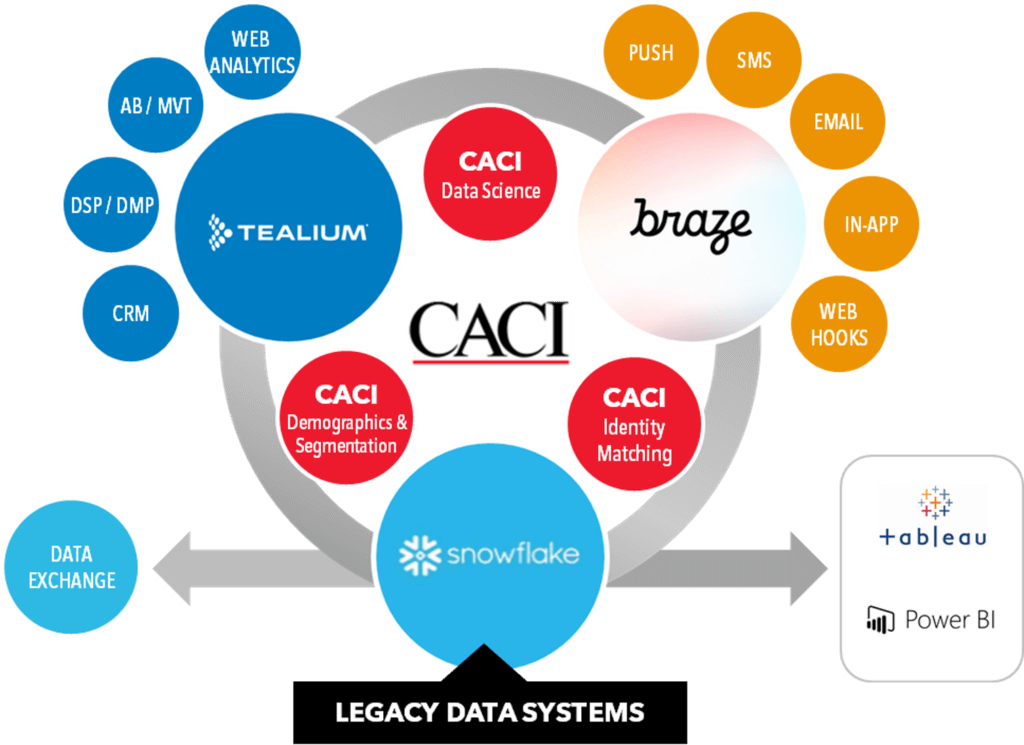

How does CACI support a firm’s wealth management customer journey?

Through a detailed understanding of current investor behaviour needs and growth opportunities, CACI can support businesses by quantifying acquisition opportunities across regions to inform effective growth and investor engagement strategies.

Once businesses have been equipped with the appropriate datasets to target high net worth individuals (HNWI), CACI can support the optimisation of marketing performance across channels and help businesses improve their distribution performance through digital, direct and intermediated channels to drive improved marketing return on investment, increased customer acquisition and better investment retention performance.

CACI offer a range of support for wealth managers and firms to meet customers’ needs while ensuring compliancy, including:

- Support in better understanding existing investors.

- Understanding the market and identifying opportunities, particularly in identifying how and where to acquire HNWI.

- Determining where potential and current customers are located, as well as their value.

- Receiving demographic data and behavioural insights on investors to better understand the customer landscape.

- Demonstrating compliance with Consumer Duty, with meeting customers’ needs remaining at the heart of what CACI do.

How CACI use data science & analytics to support the wealth management customer journey

CACI’s data science & analytics services have three primary capacities to support the enhancement of the customer journey:

- Using pre-existing information on younger investors in wealth managers and firms’ portfolios to build bespoke datasets. CACI’s multi-sector knowledge and access to unique lifestyle datasets enables the building of this bespoke consumer data insight, providing wealth managers and firms with a detailed picture of the opinions, preferences and spending potential of HNWI.

- Modelling prospects for HNWI based on demographics.

- Assessing firms’ historic data to determine how HNWI already in their portfolio achieved this position by tracking their movements and identifying signals and triggers, to enable modelling of future investors.

CACI’s wealth management customer journey support: real-time examples

How CACI’s Fresco solution supported one business’ customer acquisition & marketing strategy

CACI’s Fresco solution was employed at one business to establish a granular understanding of existing investors. This allowed for the development of a targeting propensity score, which enabled the pinpointing of potential investors that would be most likely to join the business. CACI then identified and mapped opportunities across the UK, considering regional differences and high value areas to target. Detailed insight into prospects supported the development of a consistent marketing targeting strategy within the business, which was also rolled out across traditional and social media.

Results:

- Development of a targeted audience strategy focusing on high propensity and high value audiences.

- Reduction in digital marketing spend.

- Increase in digital marketing ROI (return on investment).

How investor segmentation, personas & geographic data application transformed a business

CACI developed investor segmentation, detailed personas and geographic counts to support a market sizing initiative requested by one client.

The resulting data uncovered hundreds of variables at an individual level and provided rich insight into a range of traits and characteristics. This not only supported the business’ understanding of its current customers, but of the wider UK investment market. CACI developed personas to help the business gauge an in-depth view into consumer behaviour, insight into the market and the potential reach for key segments. Finally, geographic mapping helped the business understand acquisition and growth potential across catchments and regions, and cross-sell models were developed to support the immediate activation of distribution and marketing activity.

Results:

- The business experienced steady and sustainable growth in its acquisition, retention and reactivation.

- Increased investment values were received from both new and existing investors.

- The business was equipped with actionable insights to help inform ongoing and future marketing and office location strategies.

Throughout this blog series for the wealth management industry, we break down the opportunities for businesses to attract and retain high-net-worth individuals. Continue reading at the links below:

Blog 1 – Four barriers wealth managers face when attracting & retaining customers

Blog 2 – How to identify, attract & retain high net worth individuals

Blog 3 – Three reasons why wealth & asset managers need young investors

Whitepaper – Acquiring new high net worth clients – What wealth managers need to know

To find out more about how CACI can support your wealth management customer journey, contact our team of data experts today.