Objective basis for strategy and resource allocation

About Northumberland County Council

Northumberland County Council looks after a population of over 320,000, in England’s most northerly county. Northumberland is one of England’s five largest counties, with widely distributed towns and communities of varying types and populations.

The Challenge: Understanding the needs of different neighbourhoods

Senior Economic Analyst Julie Dowson provides data to departments across the council, from housing and planning to public health and regeneration. She says:

“Our communities have such wide differences – it’s really important to look at them at a granular level and compare them. That’s where the Paycheck data comes in. We need current, household level information to understand exactly where people are experiencing challenges, so the council can target plans and funds to address them”.

The Solution: Household-level Paycheck data reveals areas of need and opportunity

Northumberland County Council also uses Paycheck insight to feed into its annual Economic Performance Assessment and five-year economic strategy. Julie says, “You can’t plan based on subjective assumptions – the Paycheck data provides objective evidence to support our policies, priorities and programmes. That means everyone in the Council as well as our partners and customers can see and understand why we’re focusing our resources in particular areas.”

The Benefits: Targeted help and support for towns and communities

Northumberland County Council used Paycheck data to inform its Local Plan. The outputs influence Strategic Housing Market Assessments and Land Assessments, which identify potential locations for additional housing and indicate what land may be released for future housing development. This helps Northumberland County Council to plan enough affordable homes to meet residents’ needs in different housing developments across the county.

Accessible, visual information for a wide audience

About Dumfries and Galloway Council

Dumfries and Galloway Council is responsible for the delivery of all local authority services to nearly 149,000 people living in both urban and rural areas in the southwest of Scotland.

The challenge: Understanding the needs of different neighbourhoods

Gregor Docherty is Dumfries and Galloway Council’s Economic Development Officer. He explains: “Although we have some data of our own, we don’t have the range and breadth of it to provide the information the council needs today. I was given the challenge of improving our data insight, to give us a clearer view of the areas the Council looks after and the needs of the people who live there.

The solution: CACI’s data provide valuable insights

Dumfries and Galloway Council has access to Paycheck income data for two years. Recently, Gregor decided to add the Household and Wellbeing Acorn datasets to the subscription.

The addition of Household and Wellbeing insight provides a granular picture of lifestyle, income and risk factors at a local level, so we can really examine areas of need and deliver value and impact from the council’s services and programmes.

The benefits: Clear, trusted and detailed insight into household income change

Dumfries and Galloway Council successfully applied for Borderland Inclusive Growth Deal funding, using information modelled from CACI’s data. Gregor created a Dumfries and Galloway datazone profile, bringing together all the available information to rank the towns in the Council’s area for funding priority. The analysis revealed the four priority towns for funding, which was approved.

As with every industry Grocery Retail has had to adapt to a seismic shift in consumer attitudes and behaviour.

And those attitudes and behaviours continue to shift in response to local, national and even global events. The consumer has weathered the pandemic but is now staring down the challenges borne out of a cost of living crisis.

So, you need to make important decisions, and quickly. Flexibility is key. Having the data and tools at your disposal to make anything from adjustments that impact fine margins, right up to transformational change, is essential.

An innate understanding of your customer – their attitudes and behaviour – gives you the insight you need to attract new customers and retain existing ones. It’s also the foundation to building strong brand loyalty, even in challenging times.

CACI know more about your customers than anyone else. We combine a market leading demographic classification system with highly detailed footfall and spend data to provide you with everything you need to know about the way customers interact with your brand, your locations, and your competition.

For confident decision making, for greater market share, for sustainable and accelerated business growth – make your strategic location intelligence partner CACI

Strategic decisions need strategic insight

CACI offer unrivalled insight into the fundamental relationship between people and place. Understanding this relationship speeds up decision-making and minimises risk from Cap Ex investment.

We are supporting grocery retailers with insight on:

How customers engage with your brand in a physical and digital environment

The demographic profile of the catchment of each of your stores

The spend potential of the catchment in any location

The shifts in footfall and spend across times of day

The profiles of customers engaging with your competitors

Other locations similar to your best performing sites

Data driven network expansion driving the most ROI

Creating the right formats for the right locations to serve the local communities

At the end of this work, we had a growth plan to refer to, which meant we could prioritise and focus incoming opportunities. With tangible, data-led evidence and a well-defined process and criteria, we could make decisions more quickly

MidCounties Co-operative

Unprecedented insight into the grocery retail market

Understanding the way customers interact with your brand, and how potential customers engage with your competition, is the first step to increasing your market share.

And with a complete view of the competitive landscape both nationally and locally, you will have the tools you need to develop strategies for success.

At a customer level you can:

Discover the demographics that are drawn to your brand

Discover those that aren’t and why

Find out when they spend, how much they spend and what they spend their money on

Drive customer loyalty and win larger share of wallet

Identify highest spending customer groups and locate more of them

At a location level you can:

Find out where your current and potential locations rank in terms of spend

Benchmark locations against a national average across a range of criteria

Model catchment areas and market share catchments

Forecast how a particular location will change over time factoring demographic shift

Understand your local market share and competitor spend

Identify key growth opportunities in your store estate

Inform partnership strategy to generate greater footfall

Measure impact of your and competitor activity, e.g. marketing, store refurbs, etc

The CACI Consumer Spend Data has been instrumental in Sainsbury’s breaking new ground in our understanding of the evolution of multi-channel grocery. With it we can now observe changes in consumer spending and preference across channels at both national and local level and can see market dynamics play out in near real-time

Sainsbury’s

The analysis to understand the digital / physical dynamic

The relationship between physical and digital has evolved, and demographics more inclined to visit a store are now comfortable online.

How has this affected your store network?

And how does online halo impact your performance across your physical store network?

Different demographics behave differently and will even favour different brands for different channels.

CACI can make sense of this and measure the success of each of your locations well beyond just what goes through the tills. Your best performing site might not be so obvious!

Optimising your store network with this analysis in your hands allows you to make the right decisions without negatively impacting on your multi-channel revenue lines. Future proof the business by effectively forecasting online as well as in store grocery demand.

Get in touch with us to show you how we do amazing things with data.

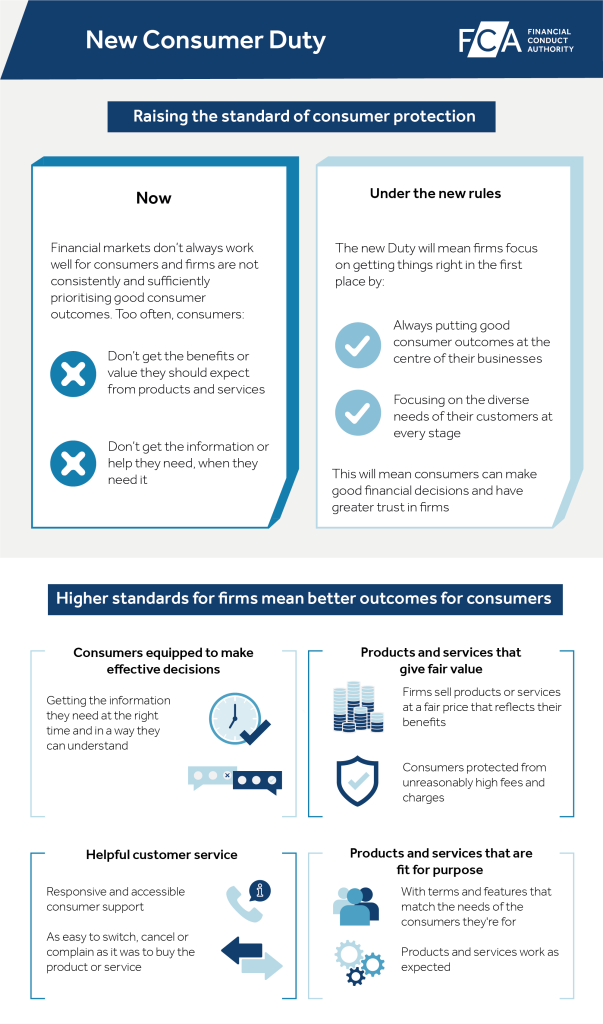

New plans from the Financial Conduct Authority (FCA) for increased consumer protection for financial services users, through a “fundamental shift in industry mindset” are to be confirmed by the end of July 2022.

The proposals include a new Consumer Principle that “a firm must act to deliver good outcomes for the retail consumers of its products”.

The regulator’s Consumer Duty directive is the latest in a series of measures tackling consumer needs in the financial services and wealth management sectors.

But how do the latest rules impact wealth and asset management firms? And how can a more effective use of data help firms increase customer knowledge and drive business growth, while ensuring compliance with the Consumer Duty?

How does the Consumer Duty impact wealth management firms?

Banks and building societies have moved steadily towards digitisation and customer-first policies over the past decade, but the wealth and asset management sector hasn’t moved as quickly.

While some firms have already adopted a business model that enables customer-led and technology-enabled strategy, it is only in the past 18 months that the importance of a data-led approach to wealth management has become prominent – and many firms are still playing catch-up. The Consumer Duty may well act as a catalyst for many to speed that change along.

The FCA is worried that, currently, financial services do not always work well for consumers, who are buying products and services that are not always fit for purpose, and not continuously receiving the best customer support.

Consumer Duty creates a shift towards making firms more proactive about the suitability of their products and services, to directly meet the needs of those they are sold to.

Wealth managers, along with other financial services firms, will need to improve consumer understanding, review the entire consumer lifecycle and journey, revisit how and what to include in customer marketing, and establish new ways to measure all these areas, in order to remain compliant.

“The new duty will drive a change in culture at firms. We expect firms to step up and put consumers at the heart of what they do, and we’ll be holding senior managers accountable if they do not.” warned Sheldon Mills, Executive Director of Consumer and Competition at the FCA.

Customer marketing – who are the new prospects?

Clearly, the FCA wants firms to better understand their customers. But how do wealth and asset managers do that? What steps do they need to take to make their business fit for purpose in a digital world and comply with Consumer Duty?

Regulatory pressure provides an opportunity to capture the market – collecting data and enriching it in order to tailor distribution and marketing.

Wealth managers are seeing changes in both customer behaviours and types of customers, and are moving away from the traditional investor to hunt out wealth in other areas – as they fight for market share. Meanwhile, fintech disruptors are raising the bar with innovative offerings.

Consumer insight is key. Young investors who are creating or inheriting their own wealth are increasingly important, as the older consumer market depletes. They are joined by more entry-level investors – and both personas have very strong customer service expectations.

These younger, and often more knowledgeable, investors are the customers of the future. They know they can invest quickly and easily online and they expect the same level of speed and ease of use in all their financial dealings.

A data-driven customer experience

Firms need to better understand the current and future needs of investors, those who might have a sophisticated, historic book of customers, now need to reach a broader audience – and CACI can help firms do that.

Consumer Duty firmly indicates products need to suit their customers, and firms need to be where investors can see them in order to market more broadly. Changing expectations might include more sustainable or green investments.

Those firms that recognise the need for better customer understanding are starting to bring in people with wider customer-first experience from other industries – increasing the sector’s pool of knowledge.

It is key to firms’ long-term growth that they do more with consolidated data – because if they don’t, they can be sure their competitors will. Firms will have data on customers, but many don’t know how to make the most of it.

At CACI we can help firms:

Understand their customers

Understand the market and identify opportunities

Know where potential and current customers are located, and their value

We can help brands across the wealth management, asset management and financial services space with demographic data and behavioural insights on investors.

Wealth and asset management firms looking to grow their business need to consider the importance of over- arching information and scalable transformation. Rich demographics on lifestyle, attitude and behaviours in the investment market, can empower better target distribution activity – driving revenue growth and increasing client engagement.

CACI will:

Provide detailed understanding of current investor behaviour needs and growth opportunities

Quantify the acquisition opportunity across regions to inform growth and investor engagement strategy

Enable optimisation of marketing performance across channels

Improve distribution performance through digital direct and intermediated channels

Demonstrate compliance with Consumer Duty to show that they are looking at, and understanding, customer needs

The new Consumer Duty is an important directive from the FCA to protect consumers. It recognises the need to focus on consumer outcomes and to put these outcomes at the heart and centre of the organisation.

For financial services organisations to achieve the requirements of the Consumer Duty, there is a need for change. Change will require overcoming common obstacles around data, communication plans, marketing goals and working practices.

To be in line with the Consumer Duty, firms need to know their customer, adapt their products, and use data to drive messaging.

CACI is here to help

The result is that Financial Services organisations will need to improve consumer understanding, have a complete view of the consumer lifecycle and journey, revisit the selection and messaging used in communications, and establish new means to measure.

Operational siloes, fragmented data, incomplete consumer profiles, product-oriented campaigning, and slow/linear working practices all create barriers to achieving the FCA’s directives. Our experience has been that firms may be dealing with several of these blockers at one time, requiring more holistic solutions than a traditional agency or consultancy can provide.

CACI’s unique positioning in the market as part agency, part consultancy, part data provider and part system integrator ensures that we can really drive value for your business. Our services and data products have always been there to connect firms with their customers. Some of the ways we can help:

Enriching consumer data – Nationwide rely on CACI’s demographics and lifestyle data variables to provide deeper insights on who their customers are and the size of the market opportunity

Segmenting and insights on consumer audiences – the Money and Pension Service have used CACI’s services to build a profile of the nation’s wealth and indebtedness

Fixing data quality and fragmentation – working alongside their own data teams, CACI are improving the quality, latency, and reliability of the data that Bupa holds and uses in marketing

Improved marketing and communications tools – Virgin Money have invested in market leading communication tools, CACI has designed bespoke customer journeys to leverage this new technology

New reporting and measurement – from attribution through to complex propensity models, CACI can visualise and report on the KPIs that really matter

Efficient operating models – through improvements in the people and process side of marketing operations, CACI can strip out 80% of the time required to launch a campaign from idea through to results. This will enable you to send more targeted campaigns to the right consumers

Product insights – our Retail Finance Benchmarking services provide vital insights into the market for personal loans, current accounts, savings, and mortgages which supports and enables product design, proposition development, and provides an objective measurement of market performance.

The Consumer Duty is an important directive with vital intention to build trust between financial institutions and consumers. For help with your journey to compliance, please contact either Paul Sene or Cara Bramwell to find out more.

As the country learns to live with Covid, CACI’s data and consumer research is revealing what the new normal looks like for the nursery market.

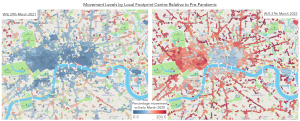

Customer Movement is on the Rise

Let’s start with the positives. Remember just how much more freedom we have than we did this time last year. The contrast between the two maps based on anonymised Mobile App data are stark. The map on the left shows movement activity levels in the last week of March 2021 relative to pre-Covid (Early March 2020) for Central London.

Source: CACI / Digital Envoy

Dark blue shading shows areas that movement levels were way down on pre-pandemic across much of London – not surprising given that restrictions were really only lifted in early April 2021 for all but essential activities (albeit including trips to nurseries). The map on the right is the same week this year, and shows swathes of red across much of London, highlighting that activity and visits to many of these areas has returned to almost pre-Covid levels as we learn to live with life after Covid.

Despite the fact that we are seeing record numbers testing positive for the new variant there is no doubt that many are back out and getting on with their lives after a painful couple of years.

New Behaviours and Attitudes

But we have emerged into a different world. The right-hand map shows that the recovery in movement is not universal. There are still clear areas of blue and lighter red in office dominated parts of the city, and around the major stations of London. The same pattern is seen in cities across our county.

Analysis of the data reveals that our city centres are only now returning to something close to what we would have called normal before the pandemic, and transport hubs are seeing visits about 25% down. But regional towns have grown in popularity, with visits up by about 40%. So, clearly we have changed our activities, and it looks like many of these behaviours are set to remain.

Our towns and cities are changing, and we can see it happening around us. But it’s a complex picture. Whilst some have speculated that we are going to witness a long-term boom in the suburbs as everyone moves out of our towns and cities – this is not the case. Despite the jolt that Covid brought there are too many interactions at play for all the old links to be broken.

CACI’s research, carried out as restrictions were eased, revealed that many 18 to 34 year olds, many in the target age groups for nurseries, were keen to return to our towns and cities. These included people from across the demographic spectrum with groups with very different lifestyles – from ‘City Sophisticates’ to ‘Struggling Estates’ in CACI’s Acorn classification amongst those most keen to return to urban living.

Consumers are listing eating out, entertainment and leisure activities as the top reasons for wanting to return.

In short, for many our towns and cities remain places of fun, choice and opportunity – and this hasn’t changed with the pandemic. What we are seeing is that towns and cities are responding to this need. At CACI we have never been so busy in supporting our leisure clients who are busy trying to extend their portfolios, filling the units vacated by retailers hit by the step change in online shopping triggered by the pandemic. And other urban offices and former retail units are being repurposed as urban living – a clear sign that everyone is not heading for the countryside and suburbs.

For many, working patterns look like they have changed for the long-term. Evidenced in the conversion of office space to other purposes and in the areas of blue on the map of central London in worker dominated areas. Our research revealed that workers claim that 2 to 3 days is the optimum number of days they would like to spend in the office, and this seems to be becoming the norm for many. But, it is important to remember that not everyone has this option, including most workers in the nursery sector. It is very easy to think everyone can work from home easily, but affluence, age, location and job role all clearly play a part.

Source: CACI / Digital Envoy

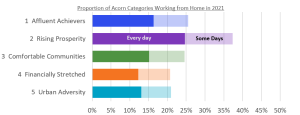

Analysing Kantar’s TGI survey data from 2021 shows that, even in a year scattered with various work from home advice, only 25% of those surveyed said that they worked from home every day, or some days, as their ‘normal’ behaviour.

The chart, using CACI’s broad Acorn Categories to dissect responses, clearly illustrates that it is the ‘Rising Prosperity’ that are most likely to be working from home. These are younger, well educated professionals moving up the career ladder and living in our major towns and cities. 38% of this segment claim to work from home at least some days, and 25% of this is made up of those working from home every day. In contrast only 20 or 21% of lower paid, lower qualified segments ‘Financially Stretched’ and ‘Urban Adversity’ have the luxury of even working from home some days.

Source: CACI / Kantar

As a result of this shift workplace nurseries will no doubt continue to suffer, as many will prefer the flexibility of nurseries closer to home, in line with the shift to ‘hybrid’ working, with many neighbourhood nurseries benefiting from this change. The number of parents requiring nursery spaces is unlikely to be impacted by the rise in home working, as many learnt during the Covid lockdowns that working from home and providing childcare don’t mix. However, many nurseries are likely to see increasing staffing and pricing complexity with parents expecting a level of flexibility that reflects the new-found flexibility in their working hours and location.

So, despite big changes there is no evidence to suggest a need for wholesale changes in where acquisitive nursery groups should be focussing their attention. The big urban to rural shift is not happening and indeed CACI’s research shows that even at the peak of the pandemic 10% of house moves were from villages to towns and cities. Tracking planning applications reveals huge amounts of new dwellings under construction or being proposed in our urban areas and, whilst much of this will have been planned before the pandemic, it’s not that easy to turn a tanker. It is simply not possible for such a shift to happen without fundamental changes in planning policy and housing stock.

So, in summary whilst the change in residential patterns are moderate it is the behaviours of those residents that have changed, and the following are just a few more key behaviour changes that CACI expect to remain:

Communities are eager to stay local

This is good news for nurseries operating well-run community nurseries. But it is increasingly important for nurseries to engage with their wider communities and larger groups need to take care not to look like corporate outsiders

Social governance is increasingly in the spotlight

With consumers expecting their suppliers to behave ethically and transparently

Minimising waste and environmental impact is mainstream

All nurseries now need to ensure that they are meeting parents’ expectations here and that they are living out the values of care for the environment that the children will inherit

Digital is critical to recruitment and engagement

There is no doubt that digital is here to stay – so if you are not happy with your website you can be sure that it is putting off potential customers and if you are not sharing key messages with your parents via emails and portals then you may get left behind

New Challenges and Opportunities

Unfortunately, with inflation and rising rocketing fuel prices, there is no doubt that many families are going to be facing increasingly tough decisions about where to prioritise their spending in the year ahead. This could impact customers’ ability to afford childcare, especially if their salaries rise above the eligibility threshold for free places, but their true disposable incomes fall.

Rising fuel costs for nurseries will compound the challenges of rising wages already driven by the shortfall in staffing that so many in the sector are facing and these need to be factored into nurseries strategic plans.

Successful nurseries should take note of these consumer and market changes, play to their strengths in these areas and they will thrive. But ignore them at their peril as the sector faces the two emerging, and partly inter-related challenges of staffing and the cost-of-living crisis.

TSB is pioneering a new kind of banking for Britain – one that’s simple, straightforward and cares about people. The bank offers friendly, honest and convenient banking that’s designed to meet customers’ needs and equip them with money confidence.

The Challenge: a segmentation to drive business growth

TSB had a creative-led segmentation developed by its brand agency to help understand its target audience, but it wasn’t fully effective. Justin Bell, TSB’s Head of Insights, Strategy & Planning explains:

“We couldn’t use it for media planning and it couldn’t be overlaid on our customer base.

We knew we needed something more practical in terms of consumer insights and choices of media. At pitch, our new media agency the7stars, came up with a more effective segmentation that we could use for media selection. We wanted to take this forward another step and overlay it onto our own base. We had for some time been working with CACI, mapping their Fresco financial lifestyle segments onto our customer base. We therefore initiated a joint project, working with CACI and the7stars to develop the segmentation further.”

The Solution: accurate, current segmentation that reflects consumer behaviour

Working in collaboration with TSB’s Research and Strategic Insights Team, CACI created an evolved segmentation that clearly distinguishes different customer types and provides clear segment profiles and personas.

CACI used Fresco and other external consumer demographic datasets to give TSB bespoke behavioural and lifestyle insights into its target customer base.

Justin explains, “We started with a market-wide segmentation, based on all UK adults. We’ve subsequently created a version of that for our customer base.

CACI provided a proven methodology and approach drawn from their data expertise and experience. Once we had clear segment parameters, our data team mapped them to our base.”

The Results: tailored propositions, content and media selection

TSB is actively using the segment insights to develop its media strategies and in campaign briefs, creating content tailored to target consumers’ profiles.

Justin continues:

“Part of the output of the segmentation was to rank the segments in order of money confidence. Working with CACI, we agreed on a weighted mix of key questions in the TGI consumer survey, to derive a money confidence score. We support people with content, products and services to help raise their money confidence and we need to be relevant to those that need that support most.

At the heart of it is a money confidence score: we’ll measure our progress against our purpose: Money confidence for everyone everyday. We hope to see a gap opening up between the money confidence levels of our customers and that of non-customers, with a continual improvement against today’s baseline.

We believe this segmentation will continue to pay dividends as we develop our channel and campaign marketing – we’re looking forward to tailoring products and services even more to meet customer needs.”

Jonathan McDougall-Bagnall is the Planning Innovation and Infrastructure Manager at the University. He explains: “The data project is part of our Contextual Admissions Policy launched several years ago. We are constantly striving to widen access to our institution and ensuring that it remains accessible to all. Historically we have used SIMD (Scottish Index of Multiple Deprivation) data and school performance data to identify candidates in Scotland who may require the support of our contextual admissions policy. We wanted to widen this to applicants from around the UK and needed to find suitable equivalent data. Each UK country calculates their index in a slightly different way, so we couldn’t make a direct comparison.”

The solution

The St Andrews team researched the data sources available and concluded that Acorn was the most comprehensive, accurate and current dataset for their needs.

“We use the Acorn postcode database as an integral part of our decision making system, to help us determine which candidates come from areas of deprivation,” says Jonathan. “We have the database and the profiler software, though we mainly use the database directly. The data is simply structured and easy to use, it comes in the same format every year. It’s very straightforward to pull into our systems, because of the consistent format and quality.”

The benefits

Joanna Fry, Access Manager: Widening Access & Transitions, says, “Our admissions system includes codes attributed to socio-economic deprivation and other widening access criteria, drawn from Acorn data and other sources.”

“Both the admissions team and our academic colleagues can now look at students in groups and compare peer groups of those with similar access codes. This gives us vital context to benchmark students from similar environments and circumstances. For example, it can help us interpret the range of exams they’ve taken; the candidate’s school may not have a wide range of subjects on offer. It also can help us understand how personal statements and references are written, depending on the influences and level of support that a candidate may have had.”

We want students with the best potential; the Acorn data helps us identify potential that goes beyond certified grades. We have plenty of evidence to show that students can do extremely well even from constrained academic and teaching backgrounds. If we understand the area and school that candidates come from, alongside their grades, we have a much clearer picture of their ability to perform.

Joanna Fry, Access Manager: Widening Access & Transitions, University of St Andrews

Download the case study

Click here to view the full customer story. To find out more about how CACI can help you support your organisation, please get in touch.

The opportunity for Landsec to re-engage customers and their spend as we emerge from the pandemic is substantial. 2020 saw the greatest level of consumer disruption ever seen in living memory with mandatory retail and leisure closures, stay at home orders, and schools and offices closing.

Landsec’s key questions included; who is driving performance, where they are coming from, how much are they spending per category, what they are doing in centre, and how are they engaging ? This helped the Landsec team identify why guests have reengaged and how to influence future behaviours. Tracking information was also used to provide the data points needed to allow Landsec to measure ROI on marketing and leasing activity.

The solution

CACI’s solution used transactional spend and mobile data to track real life actual behaviour in the centre. Mobile data looks at GPS tracking from mobile apps and helped Landsec understand the visitation patterns.

Transactional spend data is derived from credit and debit card spend data from multiple sources, including top UK retail bank and credit card companies. Again, this data was used alongside CACI’s data sources to and understand which categories and brands were driving spend and transactional changes.

Catchment spend for all the centres was also tracked using the transactional spend data, as well as a valuable indication of online spending for the centres’ shoppers.

The benefits

The data was used by the Landsec centre teams to fully understand the immediate impacts of the pandemic and how the centres performed over this period. In addition the research gave them an understanding of how best to react to the easing of future lockdowns in 2021. The research is now being rolled out across the whole of 2021, to track performance on a regular basis for some of Landsec’s key assets.

Read the case study

Read the full customer story here. To find out more about how CACI can help you support your business, pleaseget in touch.